Trending Assets

Top investors this month

Trending Assets

Top investors this month

Selling Illumina, Buying Pacific Biosciences

Two days ago I wrote about why I think my thesis with Illumina is broken. I will be buying three companies to replace Illumina. The first is Pacific Biosciences of California. Here's why.

Genomics is an exciting area, but also one that most investors have zero experience in, so I'm going to be defining some basic terms to help build up our mental modal bit by bit:

Base pairs form the building blocks of the DNA double helix and contribute to the folded structure of both DNA and RNA.

A read is an inferred sequence of base pairs corresponding to all or part of a single DNA fragment.

To get a complete picture of a genome, you must assemble the reads. Two different techniques to do this are short-read sequencing and long-read sequencing. Illumina products NovaSeq, HiSeq, NextSeq, and MiSeq are all short-read instruments.

Short read sequencing provides high accuracy, but only small snippets of data, giving an incomplete picture.

Traditional long-read sequencing offers a bigger picture but lacks accuracy, making it difficult to tell the difference between true biological variation and errors.

But the space is evolving rapidly.

PacBio developed a new highly accurate long read sequencing technique, called HiFi. The Hifi sequencing method yields highly accurate long-read sequencing datasets with read lengths hundreds of times the lengths of short reads and accuracies greater than 99.5%.

This creates a whole new paradigm for DNA sequencing, combining the best parts of short reads and long reads into a single, easy to use technology.

With easy library preparation and faster compute times Hifi sequencing also yields quicker results.

HiFi can enable us to tackle the biggest and most complex genomes, no matter what field we’re exploring. I am most excited about human health and disease advancements, but there are other applications as well in agriculture, conservation, and microbiology.

Why Invest in Pacific Biosciences?

Up until now, Illumina's short-read sequencing was the de facto solution because it was the most cost-effective, the most accurate, and the best supported by a wide range of analysis tools and pipelines.

But in August there was a contest held by the FDA to evaluate which were the best methods for human genome variant calling.

The term variant is increasingly being used in place of the term mutation. Variant calling is the process by which we identify alteration in the most common DNA sequence.

PacBio HiFi reads outperformed both short reads and noisy long reads done by Illumnia and Oxford Nanopore machines.

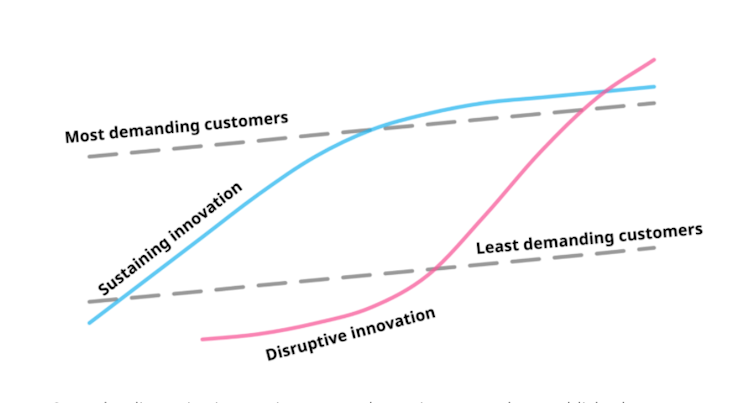

llumina's technology, in my opinion, is a sustaining technology, which means that it is improving at a rate that keeps Illumina's most demanding customer's happy. PacBio's Hifi technology is a disruptive technology, which I think has just turned the switch and is now improving at a much faster rate.

Here's the mental model to use to think about this distinction:

The market is starting to notice this change, which is why Pacific Biosciences is up 222% in the last three months. While this increases risk, $PACB is also down -6.48% today, so note the volatility.

If you're looking to get some exposure to the genomics space, I think Pacific Biosciences is a good addition to your portfolio.

PacBio

In precisionFDA Challenge, PacBio HiFi Reads Outperform Both Short Reads and Noisy Long Reads - PacBio

In the recent precisionFDA Truth Challenge V2, which evaluated methods for variant calling in human genomes, approaches that use PacBio HiFi reads delivered the highest precision and recall in all categories: genome-wide, specifically in difficult-to-map regions, and in the major histocompatibility complex.

Already have an account?